Modern Markets Episode 9.0 - "The Digital Dollar, A Look at Wealth Tech"

April 19th, 2020, by FomoHunt

You can listen to this episode on all popular platforms at Anchor.FM

Modern Markets is deeply interested in the stories of readers and how COVID-19 has affected their daily lives. Please reach at modernmarketsinfo@gmail.com if you or someone you know has been directly affected.

NOT FINANCIAL ADVICE

Coronavirus (COVID-19) Updates:

Stats via Johns Hopkins, Confirmed Cases - 2,375,443 Total Deaths - 164,716 Total Recovered - 611,430

“The states and cities, especially the ones hardest hit, like New York, should not be asked to spend a dime on this when they’re going through an economic crisis of their own.”

- Congressman Max Rose of New York

Modern Markets

Version 9.0

Modern Markets is deeply interested in the stories of readers and how COVID-19 has affected their daily lives. Please reach at modernmarketsinfo@gmail.com if you or someone you know has been directly affected.

“The states and cities, especially the ones hardest hit, like New York, should not be asked to spend a dime on this when they’re going through an economic crisis of their own.”

- Congressman Max Rose of New York

Round the World in Markets - Trouble Incoming

North America

The International Monetary Fund (IMF) has begun to forgive large amounts of foreign debt. 25 of the poorest countries in the world are seeing their debt forgiven by their lenders. IMF Managing Director Kristalina Georgieva stated. "This provides grants to our poorest and most vulnerable members to cover their IMF debt obligations for an initial phase over the next six months and will help them channel more of their scarce financial resources towards vital emergency medical and other relief efforts.” Similarly, the World Bank is distributing $160 billion to 76 countries to help combat the effects of the coronavirus.

South America

Ecuador’s issuer default credit rating has been downgraded to a “C.” The Fitch ratings company made the decision as Ecuador is exploring options to defer payments on billions of dollars in bonds that will mature this year. The low credit rating signifies a higher risk of default as the country struggles with the COVID-19 pandemic.

In a rare move, Ecuador has taken to selling 3 million hectares of its rainforest to a Chinese oil company. Ecuador currently owes China over $7 billion in loans, a substantial amount of its GDP. Concerns have been voiced by indigenous peoples groups, claiming that the oil companies will continue to damage and pollute the affected areas.

European Union

Vehicle sales have plummeted over 50% in the EU over the last month. Sales of cars and trucks hit record lows with Fiat Chrysler being hit particularly hard with a drop of 76.6% in gross sales. Financial forecasters are hoping for a “V” shaped recovery in the coming months, though a resurgence or second wave of coronavirus cases could delay that recovery by up to a year.

Africa

South African Airways has made the decision to fire all 4,700 of its employees. The 86-year old travel provider appears to be shutting down due to the lack of travelers. As a state-owned company South African Airways has been struggling over the past decade, hiring 9 CEOs over the past 10 years in its attempts to restructure and retain profitability. It has not released financial statements over the last 2 years, likely due to fears of liquidation and an inability to pay back loans.

Asia

The World Bank projects a slump in growth in South Asia. A combination of a drop in tourism, supply chain disruption, and a drop in demand for textiles are most likely the blame for the drop in revenue across several nations. The Maldives is expected to be hit especially hard, with an estimated drop in GDP of up to 13%.

The Digital Dollar

(Image Courtesy of: verdict.co.uk)

One provision that was not included in the last three stimulus plans was the Digital Dollar proposal. This proposed legislation would establish a new form of currency in the US, equivalent to one dollar.

The majority of dollars in the US are already digital and the coronavirus has been shown to be transmitted through physical currency. This seems like the perfect storm in which to transition to a more digital market. This new digital dollar would be controlled completely by the FED and its banks, of which there are twelve.

Instead of using traditional wire transfers or ACH payment methods, the new dollar is hypothesized to utilize a blockchain infrastructure. This would allow payments to be processed instantly, or at the most, within seconds. Interestingly enough this plan is already in place. In February of 2019, the Federal Reserve announced its FedNow initiative which promises instant payments across a variety of platforms:

Processing individual credit transfers valued at $25,000 or less in real time (within seconds) on a 24x7x365 basis

Settling payments through debits and credits to balances in financial institutions’ master accounts at the Reserve Banks, with an end-of-day balance recorded for each day of the week

Providing liquidity through intraday credit on a 24x7x365 basis under the same terms and conditions as for current Federal Reserve services

Implementation

What would this payment system look like to the everyday consumer? First off it would establish a new standard for banking in the US and internationally. Banks would still operate as traditional brick-and-mortar establishments but it would also allow a new generation of the unbanked to have access to the financial system. Presumably, every internet-connected device would have a digital wallet, called “FedAccount,” similar to a cryptocurrency wallet, which would allow for 24/7 access to the user’s money. While services like Venmo and Paypal allow for access there are still intermediary services that operate in the background which can limit the ability to send and receive funds. The new dollar would also be backed by the full confidence of the US government which means they could be used to pay for everyday expenses like rent, coffee, groceries, and gasoline. Loans and payments could be made directly from the wallet with a much lower cost than traditional payment, especially if dealing internationally. For example, $100 sent to Mexico through MoneyGram costs anywhere from 4-5%. On a larger scale, the reduction in fees could save companies millions of dollars in fees over time.

However, not all is rainbows and roses. If the new system does indeed utilize a centrally controlled blockchain it would mean that all transactions could be tracked by the government. In a world where most of our activities are already monitored in some capacity, this may not seem like a big deal. But for those who value their privacy, it could still raise red flags. Most of the laundered money in the world is currently through cash, and the government may cite this as a reason to move to a digital medium.

Replace Stablecoins?

The digital dollar could also be the government's way of eliminating stablecoins. Stablecoins are cryptocurrencies that are backed by the US dollar, very similar to what the FedNow program would implement. There is approximately $9 billion worth of stablecoins in the cryptocurrency market, most of which is used to purchase other cryptos of tokens.

A recent study from the G20 Financial Stability Board (FSB) has labeled stablecoins a “systematic risk” in their report titled Addressing the regulatory, supervisory and oversight challenges raised by “global stablecoin” arrangements. The report explains that while stablecoins have the potential to act as a replacement for sovereign currencies there are none that have enough market penetration to pose a threat at the moment. Any legislation against stablecoins could easily be leveraged to impact the adoption and use of other cryptos like Bitcoin and Ethereum.

No One Knows What’s Happening

(Image Courtesy of Raw Story)

The financial landscape is currently one of indecision. Despite a record number of unemployment claims, hiccups in the distribution of direct stimulus checks, and a breakdown in supply chains, the markets are booming. From a chart perspective, the stock markets appear to be going through a quick, or “V shaped” recovery. So what gives?

In the beginning stages of the COVID-19 crisis, a wave of panic overtook consumers. Many rushed to stockpile toilet paper, hunkered down with family, and stockpiled ammunition. Months later the coronavirus is a leading cause of death and the death toll has surpassed 150,000. Unemployment at a staggering 6.7%

(Image Courtesy: of Visual Capitalist)

Several pundits and analysts are calling for a recession. The International Monetary Fund (IMF) is calling for a worldwide recession in 2020 stemming from the COVID-19 pandemic. This “Great Lockdown” is projected to reduce the global GDP of 3%. Depending on how long the COVID-19 crisis continues we could easily see a recession in the upcoming months.

Surprisingly we are seeing the stock market pump from its previous lows. The S&P 500 is up from 2,190 to 2,880, though still down from the all time high of 3,390.

The consensus appears to be that the steps taken by the Federal Government have propped up the markets: stimulus checks, trillions of dollars in bailouts, lowering of interest rates, and allowing the FED to buy treasury bonds in record amounts.

Even though officials are saying we have hit the peak of COVID-19 in some states, there are still a number of factors to take into consideration. Quarterly earnings are likely to take a massive hit. Major companies like Apple and Starbucks are projecting much lower earnings or revenue as social distancing and self-imposed quarantines take their toll on sales. As the virus continues to affect our daily life it stands to reason that earnings will continue to suffer as the workforce stays at home. While President Trump is encouraging states to open up for business, the pandemic will not be over until a vaccine is produced and taken en masse. Even if a vaccine is made available within 6-8 months this is still a long time to operate under quarantine or social distancing. In a best-case scenario restaurants and movie theaters will need to operate in a diminished capacity and sporting events may see hard limits on ticket sales.

The federal government’s ability to continue to bail out these institutions over a long time period is untested. Looking at institutions for sentiment is sometimes useful to gain a better understanding of market sentiment. Interestingly, Bank of America is holding its largest cash position since 9/11. In its Global Fund Manager survey for the month of April, 93% of participants are projecting a drop in corporate earnings. Banks and other financial institutions have exponentially more information concerning the direction of the markets, which should give us a better idea of where things are actually headed in terms of equities.

Even billionaire Warren Buffet has moved to a more heavy cash position. This month he has sold massive shares of Delta Airlines, Southwest Airlines, and Bank of New York Mellon. Quite the interesting observation considering that Buffet’s advice for years has been “Be fearful when others are greedy. Be greedy when others are fearful.”

Supply Chain Disruption

(Image Courtesy of: Retail Touch Points)

The coronavirus has begun to impact one of the foundations of society: the supply chain. Supply chains are instrumental in how goods like food and appliances are shipped both nationally and worldwide. While most supply chains have redundancies for short term disruptions the current health crisis may stretch its capacity to a breaking point.

The Greenley meat production facility in Colorado has shut down until April 24th as workers and management struggle to find a solution for both social distancing and sanitary work conditions. The National Cattlemen's Beef Association (NCBA) has warned that losses in excess of $13.6 billion could ripple through the industry as other factories like Smithfield Foods and Tyson Foods cut back on operating hours. This week the Department of Homeland Security and the USDA temporarily lowered restrictions allowing foreign workers with H-2A status to remain in the country for longer than the previously enforced 3-year time period. From the USDA website: “The H-2A nonimmigrant classification applies to alien workers seeking to perform agricultural labor or services of a temporary or seasonal nature in the United States, usually lasting no longer than one year, for which able, willing, and qualified U.S. workers are not available.”

While meat production facilities are struggling to maintain production, other food suppliers are throwing out their product in actions that mirror the 1930’s. Farmers are destroying crops and dairy farms are dumping out milk that would otherwise be distributed to restaurants and schools respectively. Organizations like Feeding America and the American Farms Bureau are pushing to have these supplies distributed to food banks over the US which are currently over-extended as seeing record lines. Some food banks are seeing a 40% increase in demand as millions of people are missing substantial portions of their income due to the national lockdown.

McKinsey and Company, a business management consulting firm, has released guidelines that outline the steps that should be taken to secure supply chains during the coronavirus pandemic. These steps include establishing transparent operations, optimizing distribution capacity, and assessing realistic customer requirements. Other recommendations include digitizing supply chain management and analyzing supply chains for weaknesses and vulnerabilities. While these measures may seem like common sense, proper operations management is often difficult to achieve in even a thriving financial market. How long, and how severely, the global supply chain remains disrupted will have a dramatic impact on society moving into May.

The Rise of Wealthtech

By: Digital Lawrence

According to the world bank, “about 1.7 billion adults remain unbanked—without an account at a financial institution or through a mobile money provider.” This number has dropped from 2.0 billion in 2014, which means more and more people are coming “online” to the banking institution. For many people living in these unbanked regions, they are looking for ways to secure their wealth. I believe there will be huge growth in WealthTech products servicing these underserved communities.

You might be wondering what Wealthtech is? Well, it’s a subset of Fintech. Great, so now what’s Fintech? Fintech stands for Financial Technologies. Fintech uses technology to improve money and banking services. Typically fintech caters to savvy investors and individuals who want to have beautiful interfaces, smart mobile apps, and smoother user experience. It is an alternative to the traditional brick-and-mortar “big banks”.

Now that we know what Fintech is, WealthTech is a subset of Fintech and can be defined as by Forbes below:

Wealthtech stands for wealth and technology and is one of the subsections of fintech. Just as fintech combines finance with technology to change the way we organize, spend, and receive our money both as individuals and as companies, WealthTech unites wealth and technology intending to provide digital solutions to enhance personal (and professional) wealth management and investing.

Here in the US, there are many different WealthTech tools, you've probably heard of. RobinHood is widely considered one of the most well-known WealthTech companies today. Just as Stripe.com has opened up easy payment and billing solutions for Software as a Service company (SAAS), and Mercury.com is leading the pack with API solutions for Corporate Bank accounts, a slew of new companies are creating “infrastructure” layers for companies to build financial services on top of.

Programmable Money will become commonplace in the future. As the world’s economies grow, citizens from more and more nations will want to participate in global equities markets, alongside the burgeoning digital asset market. Wealthtech offers a more convenient way to enter these markets.

While Robinhood has dominated the US headlines, what we’re focusing on at FomoHunt is global markets - global plays.

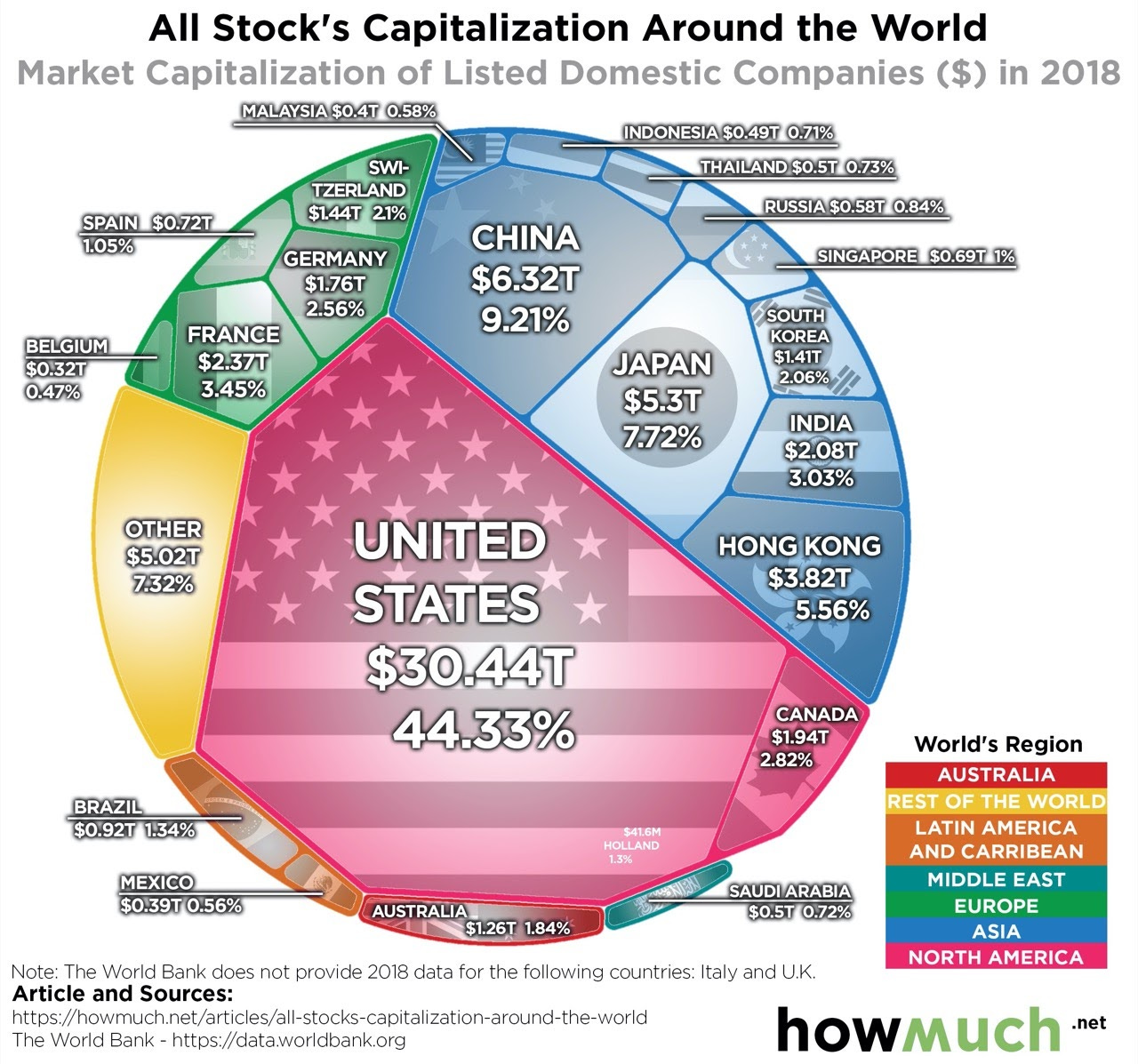

You can see from the above graphic the US stock market is massive compared to say, our southern neighbor Mexico. Not mentioned in this chart is Africa, or most of Latin America, besides Brazil. We bet that as the world “clicks” online, more citizens of these countries will want to participate in the global market, but to do so, they need the right tools. We also imagine cross-stock exchange interoperability to be coming in the next few years.

This just happened in Shenzhen, China, and Kuala Lumpur, Malaysia. Two Asian powerhouses just signed an MOU to “broaden opportunities in investment and facilitate further cross-border collaboration between the two countries.”

What we envision at FomoHunt is not only will the rest of the world enter the stock market, they will also need different ways to move money quickly 24/7. For a truly global market, this would require several mechanisms to easily move and convert local currency to assets.

For example, a Brazilian fiat on/off-ramps, cash to partner banks, into tokenized assets, and instant swaps between Malaysian stock, to a cryptocurrency, and back to cash in Malaysia.

Why is this important? Because billions of people are losing out on chances to protect and grow their wealth, by being “trapped” into their local currency.

This is what a truly interconnected world looks like to us at FomoHunt, as the rise of WealthTech products become available. This enables billions of new consumers and thousands of new businesses to participate in the global marketplace of money.

At FomoHunt we’re looking for top tools to build Financial Services for the global marketplace for both emerging and established markets. We believe in investing and we believe that there will be winners in every nation and market. Our goal is to allow anyone to participate in the next wave of financial opportunities.

Kaltoro

This newsletter, analysis, research, and commentary provided by Modern Markets, lead analyst Kaltoro, with contributions from TytanInc and Digital Lawrence. The publication incorporates data from numerous sources including, but not limited to, CoinMarketCap, Bloomberg, CNBC, Lunar Crush, and the team at FomoHunt.